Explain the Florida Closing Process: a Full Guide

Discover how to successfully navigate the Florida closing process. This guide explains everything, from costs to timelines, ensuring you're prepared!

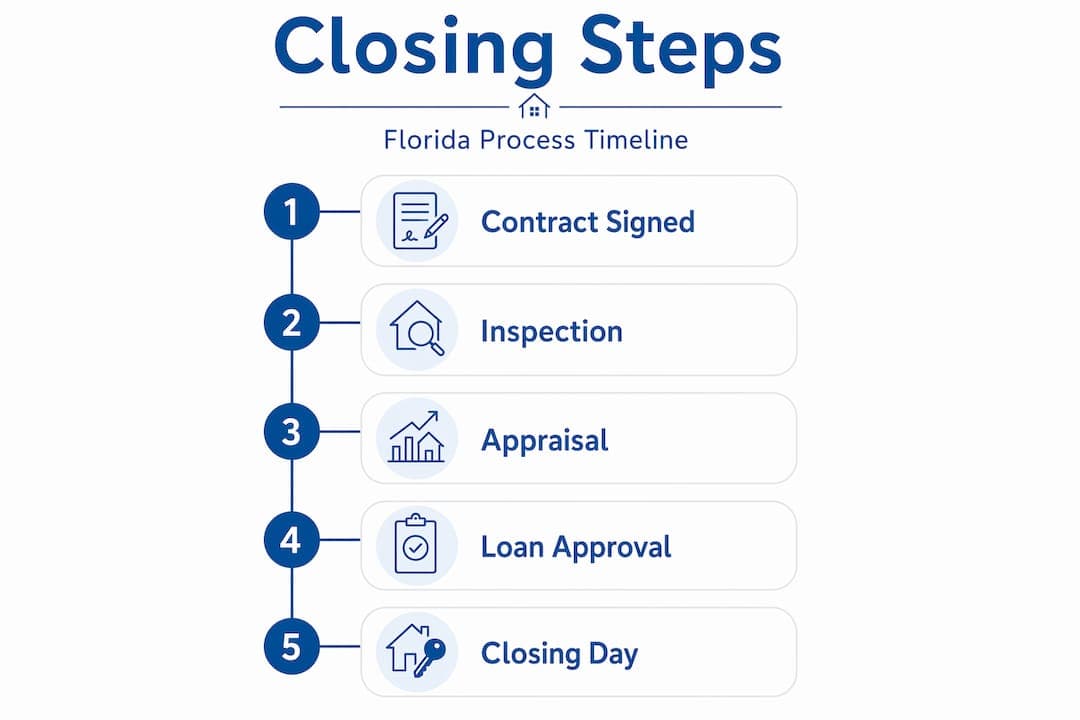

How the Florida closing process works, step by step

- Executed contract. Buyer and seller sign the purchase agreement — The clock starts now. Earnest money is deposited, typically within 3 days.

- Inspection period. Usually 10 to 15 days — The buyer hires a licensed inspector, reviews results, and either accepts the property or negotiates repairs and credits.

- Step 3 — Loan application and appraisal. The buyer's lender orders an appraisal to confirm the home's value supports the loan amount This typically takes 1 to 2 weeks.

- Step 4 — Title search. A title company or real estate attorney searches public records to confirm the seller has a clean, transferable title This process takes 5 to 10 business days.

- Step 5 — Underwriting and loan approval. The lender reviews all financial documentation and issues a clear to close This is often the most unpredictable phase.

Key Takeaways

- Contract to inspection

- 1 to 15 days

- Appraisal and loan processing

- 2 to 3 weeks

- Title search

- 5 to 10 business days

- Underwriting and clear to

- 1 to 2 weeks

Florida closing costs breakdown for buyers and sellers

- Lender fees including origination, underwriting, and processing

- Title insurance for lender's and owner's coverage

- Prepaid interest covering the days between closing and your first payment

- Escrow reserves for property taxes and homeowner's insurance

- Recording fees for the deed and mortgage

What happens at the closing appointment

- The deed. Transfers legal ownership from seller to buyer.

- — The mortgage note and deed of trust. Outlines your loan terms and pledges the property as collateral.

- — Closing Disclosure. Confirms all costs match what you were quoted. Review this line by line.

- — Affidavits. Cover items like the seller's residency status under FIRPTA if the seller is a foreign national, and lien affidavits confirming no outstanding work orders.

- — Proration agreements. Account for property taxes, HOA dues, and utilities split between buyer and seller.

Common problems that delay or derail Florida closings

- — Lender underwriting issues. A job change, large deposit, or new credit inquiry during the loan process can pause underwriting indefinitely.

- — Low appraisal. If the appraised value comes in below the contract price, the buyer may need to cover the gap or renegotiate.

- — Title defects. Unpaid liens, unresolved code violations, or estate disputes can stop a closing cold. Complex title defects often require an attorney to resolve and can add weeks to the timeline.

- — Inspection disputes. Unresolved repair requests after the inspection period can create friction that delays final decisions.

- — Wire fraud. Cybercriminals specifically target real estate transactions. Verify wiring instructions with a trusted phone call, not through email or text.

What to do after closing in Florida

- — Confirm deed recording. Your title company records the deed with the county clerk. You can verify this yourself by searching the county property appraiser's website. Typical recording time is 24 to 72 hours.

- — File for homestead exemption. Florida residents who occupy their home as a primary residence qualify for a homestead exemption that reduces assessed value by up to $50,000. The deadline to file is March 1 of the tax year following your purchase. Missing this deadline costs you real money.

- — Transfer utilities and insurance. Get homeowner's insurance active before closing day. Transfer utilities to your name immediately after. Do not leave a gap in coverage.

- — Notify your lender of your address. If you set up an escrow account for property taxes and insurance, make sure your lender has your correct mailing address for annual statements and escrow adjustments.

- — Secure your closing documents. Store your HUD-1 or Closing Disclosure, the deed, title insurance policy, and home inspection report in a fireproof location or a secure digital backup. You will need these for future refinancing, sale, or tax filings.

Skip the complexity and close on your terms

If the traditional Florida closing process feels like too many moving parts, there is an alternative worth understanding.

If the traditional Florida closing process feels like too many moving parts, there is an alternative worth understanding. Housefastcashfl works with Florida homeowners who want to sell quickly without the 45-day timelines, lender delays, appraisal disputes, or closing cost surprises that come with conventional transactions. Whether you are facing foreclosure, managing an inherited property, or simply ready to move on without the hassle, a cash offer means fewer contingencies and a dramatically shorter path to closing. You can learn exactly how cash buyers work before deciding anything. When you are ready to explore your options, get a cash offer in 24 hours and see what a straightforward closing actually looks like. Housefastcashfl also answers the question many sellers ask: are home buying companies legitimate?

Side-by-side comparison

| Buyer or Seller | Typical Amount | |

|---|---|---|

| Lender origination fees | Buyer | 0.5% to 1% of loan amount |

| Title insurance (owner's policy) | Varies by county | $1,000 to $3,000 |

| Documentary stamps on mortgage | Buyer | $0.35 per $100 of loan |

| Documentary stamps on deed | Seller | $0.70 per $100 of sale price |

| Real estate agent commissions | Seller | 5% to 6% of sale price |

| Prepaid property taxes and insurance | Buyer | 2 to 3 months of reserves |

| Title search and examination | Buyer or Seller | $200 to $400 |

Free Cash Offer

Ready to sell your house for cash?

Tell us about your property. We'll come back within 24 hours with a fair, no-obligation cash offer — no commissions, no inspection drama, no closing-cost surprises.

- Licensed Florida cash buyer

- Close in 7-21 days, on your timeline

- Free, no-obligation cash offer

- We respond within 24 hours

Cash Buyers Network

Sources & References

External sources cited in this article. Verify current figures and rules directly with the issuing source — Florida real-estate data and program rules change quarterly.

From the Blog

Continue Reading

home-selling

Inheritance Property Options: Your 2026 Heir's Guide

Explore inheritance property options in 2026: sell, rent, or move in. Learn how each choice impacts your finances and tax obligations.

Read articlehome-selling

Pitfalls of Listing Inherited Homes: 2026 Guide

Discover the pitfalls of listing inherited homes in 2026. Learn key strategies to navigate probate and safeguard your estate's value.

Read articlehome-selling

Seller Financing Rental Property in Florida: 2026 Guide

Discover how seller financing rental property in Florida can unlock investment opportunities. Learn the benefits, requirements, and legal steps.

Read articlehome-selling

Role of Heirs in Property Sales: 2026 Guide

Discover the role of heirs in property sales. Learn when you can sell inherited property and avoid common probate mistakes.

Read articleFrequently Asked

Common Questions

How long does the Florida closing process take?

+

Financed purchases take 30 to 45 days; cash transactions can close in 7 to 14 days depending on title search and coordination.

Who pays closing costs in Florida, the buyer or the seller?

+

Both sides pay. Buyers typically pay 2% to 5% of the purchase price in lender and title fees; sellers pay 6% to 8%, mostly in agent commissions and documentary stamps.

Does Florida require a real estate attorney at closing?

+

No. Florida allows licensed title companies to serve as settlement agents, but title companies cannot provide legal advice, making an attorney valuable for complex transactions.

What is the Closing Disclosure in Florida?

+

It is a federally required document that itemizes your loan terms and all closing costs. Buyers on financed deals must receive it at least 3 business days before closing to allow for review.

What causes most Florida closing delays?

+

Lender underwriting issues, low appraisals, unresolved title defects, and missed contract contingency deadlines are the most common causes. Early preparation and consistent communication with your title company reduce most of these risks.